Bonds

Bonds:

Bonds are financial instruments that represent a loan made by an investor to a borrower, such as a corporation or a government entity. The borrower typically agrees to pay back the principal amount of the loan plus interest over a fixed period of time. There are two main types of bonds:

- Corporate bonds: These bonds are issued by corporations to raise capital for their operations. They are generally considered riskier than government bonds, but offer higher yields.

- Government bonds: These bonds are issued by governments to finance their operations or fund public projects. They are considered less risky than corporate bonds, but offer lower yields.

Corporate Bonds:

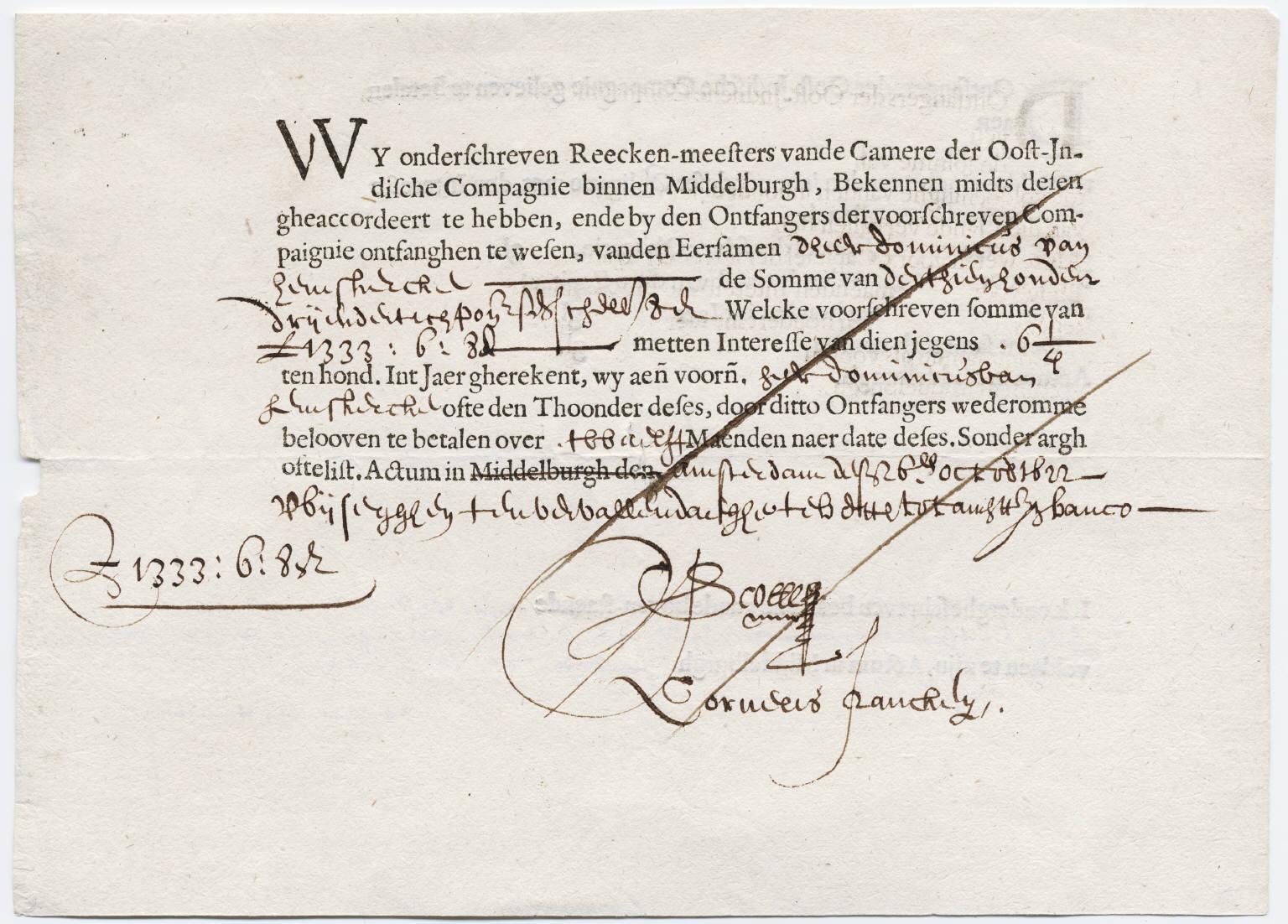

Corporate bonds have been around for a long time, with the first recorded issuance of a corporate bond dating back to the early 19th century. The Dutch East India Company is credited with issuing the first corporate bond in 1623, but these early bonds were primarily used to finance overseas trade expeditions and were not widely traded.

The first corporate bond of The Dutch East India Company in 1623.

It wasn’t until the 19th century that corporate bonds became more prevalent as a means for companies to raise capital. In the United States, railroad companies were some of the first to issue corporate bonds to finance the expansion of their infrastructure. These bonds were typically secured by the company’s assets and offered investors a fixed rate of return.

Throughout the 20th century, corporate bonds became an increasingly popular way for companies to raise funds, and the market for corporate bonds grew significantly. Today, corporate bonds are a major asset class, with a wide range of issuers and investors participating in the market.

The benefits of corporate bonds are that they offer diversification, yield and liquidity. The biggest disadvantage is that unlike government bonds, there is no federal guarantee for corporations’ debt payments. Other disadvantages include credit risk and cost of hedging. Corporate bonds are an important source of financing for businesses, but they also carry risks associated with their issuers’ ability to make their interest payments.

A corporate bond is a debt security issued by a corporation to raise capital for various purposes, such as funding operations, financing projects, or expanding the business. Essentially, when a corporation needs to borrow money, it can issue bonds to investors in exchange for a promise to pay interest on the principal amount borrowed, and to repay the principal amount at the maturity date.

Corporate bonds are typically sold to institutional investors, such as pension funds, insurance companies, and mutual funds, as well as individual investors. They are generally considered to be less risky than stocks, but more risky than government bonds, since the creditworthiness of the corporation issuing the bond and its ability to make timely interest payments and repay the principal amount depend on a variety of factors, including the company’s financial health, industry trends, and economic conditions.

Corporate bonds can have varying maturities, ranging from a few months to several years or even decades, and different levels of risk and yield. The interest rate, or coupon, paid on a corporate bond is typically higher than that of a government bond of similar maturity, to compensate investors for the additional risk. However, the yield on a corporate bond can also be affected by changes in interest rates, credit ratings, and market conditions, and may vary over time. Corporate bonds are debt securities issued by corporations to raise capital for their business operations. These bonds offer a fixed rate of interest paid to investors, and they typically have a set maturity date when the principal is repaid. There are several different types of corporate bonds, each with its unique features and risks.

Here are the most common types of corporate bonds:

- Investment-grade corporate bonds: These bonds are issued by companies with high credit ratings, typically BBB- or higher. They are considered to be safer investments because the issuing companies are financially stable and have a low risk of default. As a result, they offer lower yields compared to other types of corporate bonds.

- High-yield (junk) corporate bonds: These bonds are issued by companies with lower credit ratings, typically BB+ or below. They are considered to be riskier investments because the issuing companies have a higher risk of default. As a result, they offer higher yields to compensate for the increased risk.

- Convertible corporate bonds: These bonds allow investors to convert their bond holdings into a predetermined number of the issuer’s common stock shares at a specific price. Convertible bonds typically offer lower yields than non-convertible bonds because of the added flexibility they offer.

- Callable corporate bonds: These bonds give the issuer the right to redeem the bonds before the maturity date at a predetermined price. Callable bonds typically offer higher yields than non-callable bonds because of the added risk to investors that the bonds may be called early.

- Puttable corporate bonds: These bonds give the investor the right to sell the bonds back to the issuer before the maturity date at a predetermined price. Puttable bonds typically offer lower yields than non-puttable bonds because of the added flexibility they offer to investors.

- Floating-rate corporate bonds: These bonds have variable interest rates that adjust periodically according to a specified benchmark. Floating-rate bonds typically offer lower yields than fixed-rate bonds because of the added flexibility they offer to investors.

- Zero-coupon corporate bonds: These bonds do not pay periodic interest but are issued at a discount to their face value. Investors receive the full face value of the bond when it matures, making zero-coupon bonds a type of discount bond. Zero-coupon bonds typically offer higher yields than other types of bonds because of their discounted purchase price. Longer-term zero-coupon bonds typically have a higher discount rate than shorter-term bonds, reflecting the greater risk and uncertainty associated with longer-term investments.

Understanding the different types of corporate bonds and their features is essential for investors to make informed decisions when investing in corporate bonds. By knowing the risks and rewards associated with each type of bond, investors can create a diversified portfolio that matches their investment goals and risk tolerance.

While investing in corporate bonds can offer attractive returns, there are several risks associated with this type of investment, including:

- Credit Risk: The primary risk associated with corporate bonds is credit risk. This is the risk that the issuer of the bond may default on the repayment of interest and principal. If the issuer defaults, the investor may not receive all or any of their investment back.

- Interest Rate Risk: Corporate bonds are also sensitive to changes in interest rates. If interest rates rise, the value of the bond may decrease, as new bonds are issued with higher yields. This can result in capital losses for the investor.

- Market Risk: Corporate bonds are traded on the secondary market, where their prices can fluctuate based on supply and demand factors. If there is a decrease in demand for corporate bonds, their prices may decline, resulting in capital losses for the investor.

- Liquidity Risk: Corporate bonds may also be subject to liquidity risk. This is the risk that an investor may not be able to sell the bond when they want to due to limited market activity or a lack of buyers. This can result in the investor having to sell the bond at a lower price or holding the bond until maturity.

- Default Risk: In addition to credit risk, there is also the risk that the issuer of the bond may default on other obligations, such as payment of dividends or other debt. This can affect the value of the bond and the investor’s returns.

Overall, investing in corporate bonds can be a good way to diversify an investment portfolio and generate income. However, it is important for investors to be aware of the risks associated with this type of investment and to carefully evaluate the creditworthiness of the issuer before investing.

Government Bonds:

Government bonds have a long history dating back several centuries. The first recorded issuance of a government bond was by the city-state of Venice in 1157, to finance its wars against the Byzantine Empire. However, the modern form of government bonds that we are familiar with today can be traced back to the 17th century.

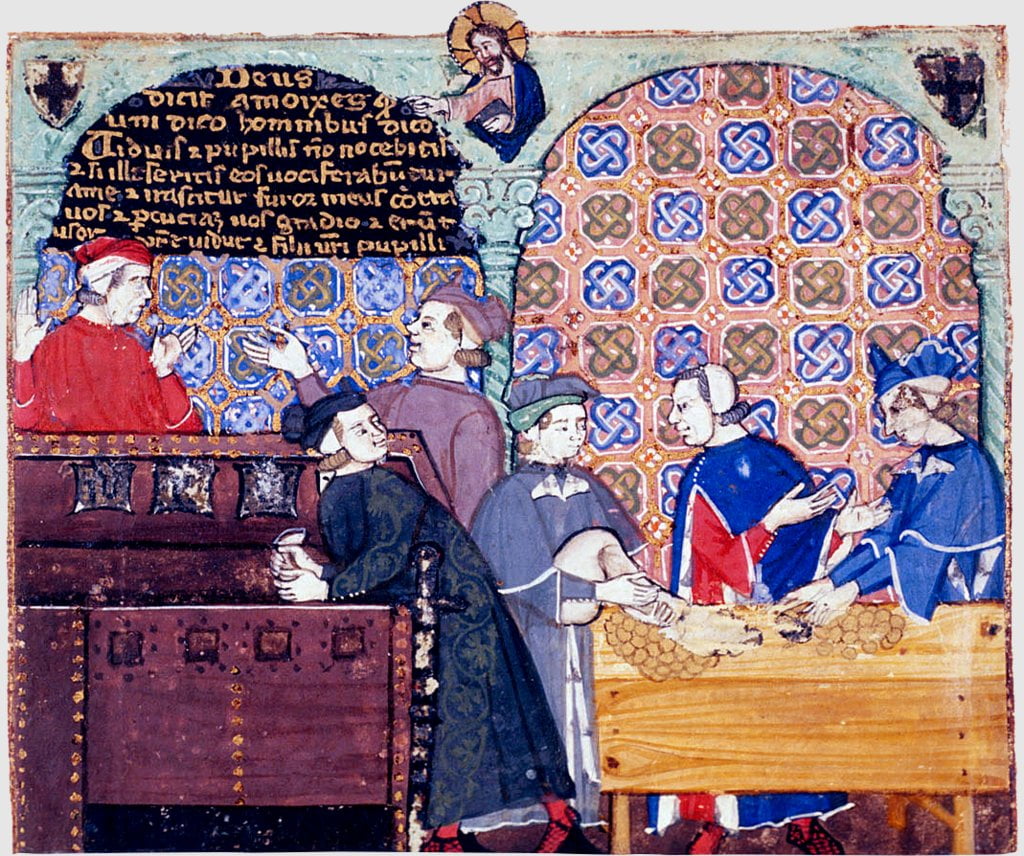

A 14th century manuscript depicting bankers in an Italian counting house.

In the 18th century, the British government issued bonds to finance its wars against France. These bonds were known as “Consols” (Consolidated Annuities), and were perpetual bonds that paid a fixed interest rate. The Consols became popular among investors and were considered a safe investment due to the stability of the British government.

During the 19th century, many European governments began issuing bonds to finance their infrastructure projects such as railways, canals, and roads. The bond markets grew rapidly, and many investors saw government bonds as a safe haven investment.

In the 20th century, government bonds became even more important as countries began to issue bonds to finance their participation in World War I and World War II. After World War II, government bonds became an important tool for financing post-war reconstruction efforts.

Today, government bonds are issued by many countries around the world to finance a variety of projects, such as infrastructure development, education, healthcare, and defense. These bonds are often considered a safe investment as they are backed by the full faith and credit of the government issuing them.

Corporate bonds come in various types, each with its unique features and risks. Here are some of the most common types of government bonds:

- Treasury bonds: These are long-term bonds issued by the U.S. government with a maturity of 10 years or more. They offer a fixed rate of interest and are considered to be very safe investments.

- Treasury notes: These are medium-term bonds issued by the U.S. government with a maturity of 2 to 10 years. They offer a fixed rate of interest and are also considered to be very safe investments.

- Treasury bills: These are short-term bonds issued by the U.S. government with a maturity of less than one year. They are sold at a discount and do not pay interest. Instead, investors earn a profit when the bond matures and is redeemed for its full face value.The difference between the purchase price and the redemption value represents the bondholder’s return on the investment. Because zero-coupon bonds like Treasury Bills do not pay interest, they are typically sold at a deep discount to their face value.

- Municipal bonds: These are issued by state and local governments to finance public projects like schools, hospitals, and roads. They offer tax-free income to investors, making them attractive to those in high tax brackets.

- Agency bonds: These are issued by government-sponsored entities like Fannie Mae, Freddie Mac, and the Federal Home Loan Banks. They are not backed by the full faith and credit of the U.S. government but are still considered to be relatively safe investments.

- Savings bonds: These are issued by the U.S. government to individual investors and are designed to encourage saving. They offer a fixed rate of interest and can be redeemed at face value after a set period of time.

Overall, government bonds are generally considered to be very safe investments, but they also tend to offer lower rates of return than other types of investments like stocks or corporate bonds.

Government bonds do carry some risks that investors should be aware of:

- Interest rate risk: The value of a bond can be affected by changes in interest rates. When interest rates rise, the value of existing bonds typically falls, and vice versa. This can result in a loss of principal if the bond is sold before maturity.

- Inflation risk: Inflation can erode the purchasing power of the interest payments and principal repayment of a bond. If inflation rises faster than the interest rate paid by the bond, the real return on the investment can be negative.

- Default risk: While government bonds are generally considered to be very safe investments, there is still a small chance that the government may default on its debt obligations. This risk is considered to be very low for most developed countries like the United States, but it is higher for emerging market countries.

- Currency risk: If an investor buys a government bond denominated in a foreign currency, they face the risk that the value of that currency will decline relative to their own currency. This can result in a loss of principal if the bond is sold before maturity.

- Liquidity risk: Some government bonds may be less liquid than others, meaning that they may be more difficult to buy or sell quickly without affecting their market value.

It’s important for investors to consider these risks when investing in government bonds and to balance them against the potential benefits of safety and stability. Diversifying across different types of bonds and other asset classes can also help to mitigate some of these risks.

In summary, corporate bonds offer a way for companies to raise capital and provide investors with a fixed rate of return, but they also carry risks associated with the issuer’s ability to make timely interest payments and repay the principal amount. Understanding the different types of corporate bonds and their features is important for investors to make informed decisions when investing in this asset class.

The discussion revisions log includes any modification made to the article. Request edits in the Wealth Waves Forum. If a reason for the revision is missing, the revision is simply a visual edit, like text formatting.

Sorry, there were no replies found.

The forum ‘Quezo Encyclopedia’ is closed to new discussions and replies.